associated information universal music group Following its newest earnings report yesterday (July 24), the corporate’s inventory worth fell by double digits, to say the least. Analysts have constantly downgraded their rankings. There’s hypothesis the music streaming growth might be in hassle.

It is all primarily based on one metric: UMG’s second-quarter streaming income.

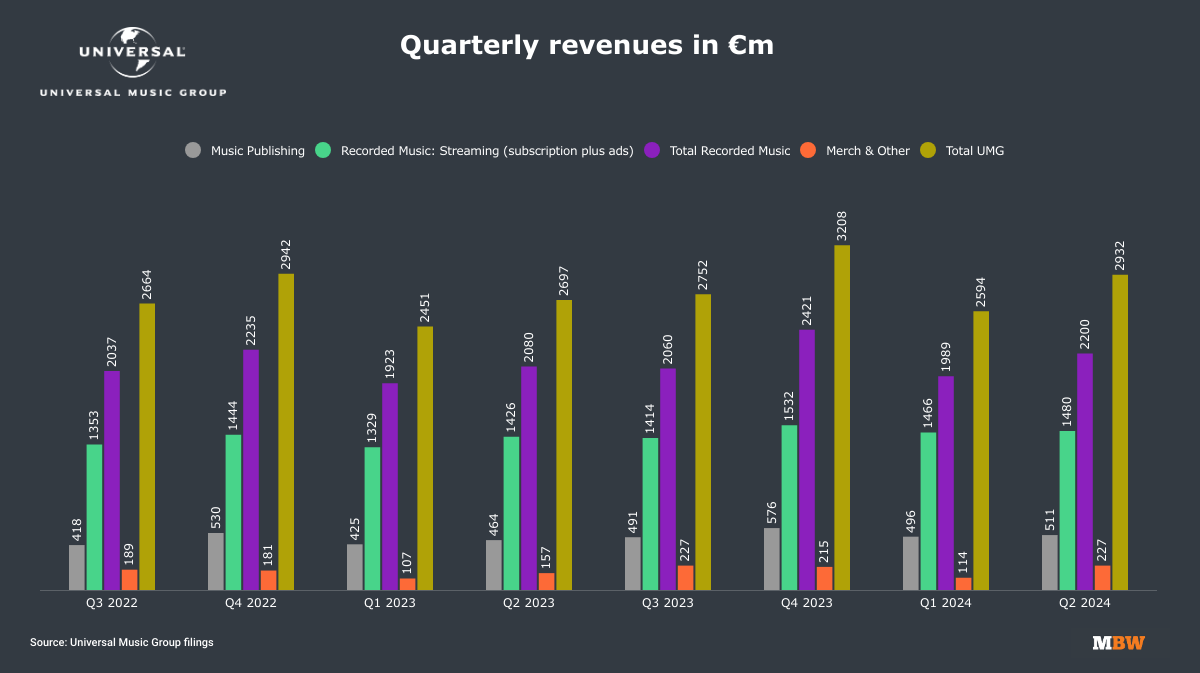

To be clear, streaming income continues to be very excessive develop exist frequent. most notably, subscription Streaming income rises Annual development of 6.9% within the second quarter – however beneath analysts’ expectations, which had been about 11% develop.

Advert-supported streaming income is in worse form, truly falling Annual development of three.9% throughout this quarter.

Nevertheless, different measures of UMG’s monetary success within the second quarter stay spectacular:

- Whole income jump up 9.6%Yr-on-year (on a relentless foreign money foundation), beating analysts’ expectations;

- Adjusted EBITDA development Annual enhance of 11.3%relying on €649 million ($699 million). This additionally beat analyst forecasts, in line with the Seen Alpha consensus;

- Web revenue surges Annual enhance of 46% Within the first half of 2024, €914 million ($991 million), or 0.50 euros per share, in comparison with 0.34 euros First half of 2023.

Nonetheless, the market was shocked. UMG shares fell greater than twenty three% At present (July 25) euronext amsterdam.

UMG additionally noticed a slew of analyst downgrades, most of which have been downgraded from “purchase” to “maintain,” together with Citibank, barclays financial institutionand Guggenheim.

It isn’t an exaggeration to say that Common Music Group’s Management Crew This appears to have been foreseen.

on Wednesday Earnings convention name, UMG executives take all of it in stride implicitly acknowledging that buyers will likely be apprehensive about declining streaming income, Present some feedback and explanations.

Maybe a very powerful of those feedback: UMG is not significantly involved about lower-than-expected streaming income development this quarter; It is enjoying an extended sport.

“Internally, we do not handle the enterprise on a quarterly foundation, so after we see modifications in our quarterly outcomes, we’re not overly involved,” stated Chief Monetary Officer and President of Operations Boyd Muir informed analysts on a convention name.

“We now have a diversified enterprise mannequin that may adapt to quarterly modifications whereas nonetheless delivering stable development at a gaggle degree.”

One other level Common MG’s Executives emphasised that rising costs for streaming providers over the previous few years often created the phantasm of weak efficiency.

Of explicit be aware this time are: Muir defined that rising costs apple music and Amazon Music What occurred greater than a yr in the past is now “Absolutely annualized” Knowledge from UMG, Meaning they now not contribute to Common’s annual development.

(The identical factor will occur within the coming quarters, with probably the most vital worth will increase in 2023—i.e. Spotify,That is Executed in the third quarter of last year. To this finish, analysts at Guggenheim Companions Michael Morris UMG’s subscriber income is just not anticipated to rebound within the third quarter of 2024 6.9% Charges from the newest earnings report. He expects year-on-year development to sluggish additional 5.3%in season 4.

“Our second quarter outcomes mirror the various efficiency of our numerous portfolio of DSP companions.”

Sir Lucian Grangecommon music group

In fact, not all contractions are Common MG’s Second-quarter streaming income development is an phantasm.

A few of them are very actual and Age Stating that sure digital service suppliers (DSPs) have disappointing subscriber numbers – though the management group didn’t identify names.

“Our second quarter outcomes mirror the various efficiency of our numerous portfolio of DSP companions,” stated UMG Chairman and CEO. Sir Lucian Grange Mentioned fastidiously.

Chief Monetary Officer Muir elaborated: “Though Spotify, Youtube Many regional and native platforms proceed to see wholesome consumer development, whereas different massive companions which have been much less profitable in driving world adoption are seeing slower new consumer development.

(You may discover, there, Spotify and YouTube Off the hook; UMG blamed weak consumer development on a few of its different “massive companions” within the digital area.

Muir UMG added, “In-depth conversations are ongoing with all of our key companions on product innovation to focus on high-value prospects and drive future income development.”

complete, grunge Emphasizing that UMG’s technique is to not chase quarterly outcomes, however to construct a powerful enterprise over the long run.

“On this lengthy interval of development, we all know that quarterly fluctuations in a single income stream or one other are to be anticipated,” he informed analysts in his opening remarks.

“In order we report our outcomes every quarter, we’re additionally managing the enterprise for long-term success. We expect in multi-year cycles and anticipate and embrace modifications in sure enterprise strains.

Listed here are 4 different issues we realized on UMG’s earnings name, together with the potential of Spotify’s new “tremendous premium” subscription tier and the tantalizing trace that UMG’s catalog could quickly be accessible in different languages…

1) Promoting income would develop with out Meta and TikTok

That is cringeworthy Annual development of three.9% If not for UMG’s two companions, the decline in UMG’s ad-supported streaming income within the second quarter would even have been a constructive quantity (i.e., better than zero): Tik Tok and meta platform.

UMG missed a month of income, executives famous on earnings name Tik Tokon the time the music large was engaged in a high-profile spat with the video platform over its funds and UMG’s recording and publishing catalog disappear from the platform.

As well as, there’s additionally the truth that meta platform Take down premium music movies Facebook earlier this yr.

“Meta has beforehand supplied high-quality music movies on Fb. In comparison with different music merchandise, this product is much less fashionable among the many Fb consumer base.

Boyd Muir, Common Music Group

“Our licensing settlement with Meta has modified when it comes to platform-specific pressures,” Muir defined.

“Meta has beforehand supplied high-quality music movies on Fb. In comparison with different music merchandise, this product is much less fashionable among the many Fb consumer base. Due to this fact, beginning this Might, Meta will now not license our premium music movies.

Muir added: “Meta is now centered on different areas involving music content material and we’re working collectively to broaden these areas as a part of a multi-faceted replace.”

2) 20% of Spotify paid customers can join the brand new “Tremendous Premium” degree

Throughout Spotify’s earnings name earlier this week, co-founder and CEO Daniel Ek Lengthy-rumored “tremendous premium” subscription tier nearly introduced Streaming service coming soon.

“Our plan is to supply a greater model of Spotify,” Ek stated.

“It is similar to 5 USD Increased than the present Premium tier…type of like a deluxe model of Spotify, with all the advantages of the common Spotify model, however with extra management, larger general high quality, and some issues I am not prepared to speak about but .

Though Ek would not go into particulars, he instructed a potential worth level of $17 or $18 per 30 days.

The Tremendous Premium tier is broadly anticipated to (ultimately) give Spotify listeners entry to high-fidelity audio, and can also embody options like a “Tremendous Fan Membership.”

We additionally performed some market analysis on the potential of this system, supplied by UMG.

“Our analysis and evaluation reveals that as a lot as 20% The present consumer base can improve to the ultra-premium tier at a considerably larger worth to acquire a compelling product configuration that gives enhanced performance and unique entry to content material,” Muir informed analysts.

View Spotify report 246 million Paid subscribers UMG estimates recommend that by the second quarter of 2024, some 49.2 million A few of them will join tremendous premium.

If the plan does price $5 extra per 30 days than the usual Premium package deal, which means US$2.952 billion Further annual revenue from Spotify. (Assume that the tremendous premium tier will price $5 greater than the premium tier in all markets, which is not essentially a secure wager.)

Assuming Spotify pays two-thirds of its income to music rights holders, this determine would characterize extra income for Spotify US$1.966 billion to the music trade.

So the tip of the streaming craze may not be right here but…

3) UMG expects 180 million potential new streaming media signups in high markets

Along with the potential of “ultra-premium”, UMG believes that there’s nonetheless loads of registration area for music streaming providers, together with in mature and developed markets.

In UMG’s market analysis, “We now have recognized an over 180 million UMG chief digital officer says that in 19 high music markets, “the following wave of subscription shoppers will type” Michael Nash Mentioned on the telephone.

“This examine was performed assuming worth will increase. Roughly half of the addressable market will likely be situated in 13 developed markets.

He stated UMG anticipated “substantial development” in rising markets.

“It is vital to do not forget that technological innovation, digital infrastructure penetration, rising client tendencies, all of those components have continued to develop the entire addressable marketplace for subscriptions over the previous decade,” he added.

Actually, the entire variety of paid music streaming accounts is 503 million By the tip of 2023, globally An annual enhance of 13.2%, In keeping with information international federation of food industry Shared by tag supply. have 667 million The variety of customers subscribing to streaming accounts in 2023 will likely be greater than double that in 2019, however nonetheless solely about 2023 8% Proportion of world inhabitants.

4) Traditional songs from the UMG catalog will quickly be accessible in different languages

Not all of UMG’s earnings name was about streaming subscription development — a few of it centered on one other of right now’s music trade obsessions, synthetic intelligence.

Current UMG announced with sound labIt’s a synthetic intelligence know-how firm that focuses on offering “ethically educated” instruments for music creators.

Certainly one of SoundLabs’ key merchandise is microphone dropa vocal plug-in that permits artists to create high-fidelity vocal fashions utilizing their very own voice information.

One results of this, in line with UMG’s Grainge, is that we’ll quickly have the ability to hear traditional songs from UMG’s catalog sung in a number of languages aside from the one during which they have been recorded.

Grange stated by telephone that UMG artists “will have the ability to sing in languages they do not converse, restore imperfect recordings, and extra.”

“The flexibility to sing in their very own voice in a language they do not converse offers us large potential and big alternatives to promote, market, unfold tradition and create demand for songs, merchandise and again catalogues, which The demand was fully achievable.

On this regard, Common Music Group may benefit from “proofs of idea” performed by different music corporations.

Final yr, South Korea transfer Launched a Korean pop music – masquerade earlier than midnight – in six different languagesbecause of the know-how developed Tremendous pitcha synthetic intelligence voice cloning firm, Ok-pop large acquired 2022.

A number of months later, Tencent MusicStreaming providers owned kugou music Kugou AIK debutswhich modifications the singing to 10 languages and 15 Chinese language dialects.world music enterprise